An aging roof that looks visibly worn down from the ground can turn into a serious roadblock when you’re trying to sell your home. It’s often the first part of your home buyers and assessors see from the curb, and if they believe it hasn’t been maintained properly, they might push you to lower the price. Licensed appraisers use simple math to calculate the reduction. Roof restoration helps you present the roof as a well-maintained asset instead.

| Time to Read |

|

| What You’ll Learn |

|

| Next Steps |

|

You’ve decided to sell, and the roof just became your biggest worry. It’s somewhere in that 15-to-20-year range: not failing, not new, and old enough that a buyer’s agent will notice at least a little wear and tear from the driveway. Should you replace it, rejuvenate it, or just list it as-is?

The answer isn’t as straightforward as you think. A full replacement can cost you $20,000 or more, and you won’t always recoup the cost by getting a better price for your home. With restoration, you’ll pay up to 80% less and get a transferrable 5-year flexibility warranty you can pass on instead.

But what are buyers and appraisers really looking for, and how much should their position on it factor into your decision? In this guide, we’ll walk you through what’s going through their minds when they consider a home, what they’re looking for, and how to honestly and persuasively position a treated roof.

Imagine that you’re shopping for a used car. Your gaze lands on two SUVs: one is in immaculate condition without so much as a scratch, while the paint on the other is faded and rusted out.

Chances are, you’ll instantly form an opinion about each one. It would be reasonable to assume that the previous owner of the “rust bucket” didn’t care for it properly or that it might have hidden problems you can’t easily see. So, if it comes down to it, you’re more likely to choose the one in good condition.

This is exactly what happens when buyers and their agents come to look at your property. Your roof is the first part of your home they see from the curb, so if it looks rough or old, they’ll automatically start scrutinizing the value of the entire property and question if you maintained it properly.

Most have a sharp eye for problems like:

A buyer who sees serious roofing issues might also assume that your roof is at the end of its natural lifespan. That might make them think they’ll have to pay for a new roof if they buy your home.

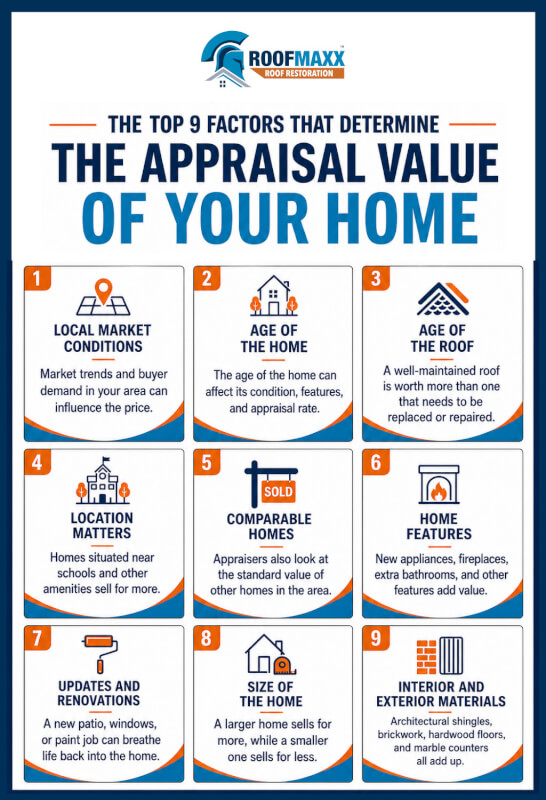

Appraisers are state-licensed professionals that are either contracted or employed by mortgage lenders (typically banks). Their job is to set a fair price for the home based on the overall condition of the property and all systems and components within it.

Unlike a buyer’s or agent’s opinion, which is informal at best, the appraiser’s findings can influence both the final sale price and any mortgage terms related to it. Depending on what they find, this can either work to your advantage or stop you from closing the deal completely.

For example, let’s say you want $200,000 for your home, but the appraisal comes in at $175,000. The buyer’s lender will only finance up to the appraised value, so they either need to make up the gap in cash, renegotiate the price down, or walk away.

If you priced the same home at $150,000, but it ends up being appraised at $175,000, the sale still closes at your listing price. The buyer just gets a bit more equity, which means they have less of a reason to push back with a counter-offer.

On the day of your scheduled appointment, the appraiser will walk around your property, photograph the inside and outside of your home, and confirm the home is structurally sound and safe. They’ll also specifically note the condition of all major parts and systems including your roof.

If they have any reason to suspect there are deeper problems, they may ask you to schedule a professional inspection so they can get a clearer picture of how it affects the value of your home.

The appraised value usually comes from the sales comparison approach. That means the appraiser starts with recent sales of similar nearby homes, then adjusts each sale price based on how closely that home matches yours.

Fannie Mae says comparable sales should be similar in physical characteristics, including condition, and the appraiser must account for factors that affect value.

For example:

That doesn’t mean a new roof would only cost $8,000. The appraiser is estimating how much the older roof changes the home’s market value compared to similar homes nearby.

The used car analogy we talked about earlier is a perfect example of this in practice. If you’re shopping for two similar SUVs, and one has minor rust on the body, you wouldn’t expect the seller to discount it by the full cost of replacing them completely. It would be reasonable to reduce it by the cost of resolving the rust.

Many homeowners assume the appraiser will inspect the roof the same way a professional roofer would, but this is rarely the case. Most will just look the roof over visually from the ground, from upper windows, and from photos rather than climbing up there on their own.

They’re also not simply subtracting the full cost of a new roof from the home’s value. Instead, roof condition usually affects the home’s broader condition rating instead.

The appraiser is looking for:

Problems like these can actually interfere with the buyer’s ability to access financing. FHA, VA, and USDA loans all generally require the roof to be in “adequate” condition with at least two years of life left in it. More conventional lenders may hold back funds until they’re satisfied that you’ve resolved any issues.

Severe damage (like a sagging roof line or large holes) may delay the buyer’s funding or even prevent the loan from being granted altogether. That’s why it’s in everyone’s best interest to put your best “shingle” forward before you sell.

Shingle rejuvenation won’t dramatically increase the value of your home, and any pitch that frames it that way is misleading. What roof restoration will do is help you make the most of the roof and shingles you already have so you (or the buyer) can put off replacement for as long as possible.

It’s a multi-step process that includes:

The end result is a roof that looks cared for, performs better, and has a documented history of maintenance that tells any potential buyers you put time and effort into keeping it in good condition.

Realtors don’t have the luxury of being wrong about the condition of a roof. If the shingles on a property look even slightly worn down or dried out, buyers will start asking questions, walk away from the sale, or use it as an excuse to argue for lowering the price.

When issues like these come up in inspection, top Realtors trust Roof Maxx to help them resolve it so they can save the deal without forcing the homeowner into an expensive total replacement.

Hear what they have to say about roof restoration in the video below:

Once your roof has been treated, the next step is making sure buyers, agents, and appraisers understand what’s been done and why it matters.

The best way to help buyers, agents, and appraisers understand the benefits of Roof Maxx is to tell them how it works and why it matters for maintaining an asphalt shingle roof. Be honest about the fact that it won’t magically fix problems like structural damage or leaks, but focus on highlighting the simple, honest benefits that come with having your roof treated.

Tell them that Roof Maxx is:

Loss of flexibility is one of the biggest contributors to shingle damage over time. Brittle shingles are more likely to crack, lose granules, and just generally deteriorate over time, and Roof Maxx is an excellent way to stay on top of it and get more life out of your roof.

Documentation protects you and the buyer because it keeps everyone on the same page about the work that’s been done and the condition the roof is in right now. That can prevent misunderstandings later, and in some cases protect you from a dispute after closing.

Put together a folder that includes:

Hand it to the buyer or their agent and let them know you’re happy to answer questions. Someone who can see proof the roof is still in good condition has one less reason to come back with a lowball offer.

The sooner, the better. The treatment goes on in a single visit, but the real advantage comes from having time to collect the invoice, dated photos, and warranty paperwork before buyers and appraisers start asking questions.

Lowering the price to cover a roof concern usually costs more than the treatment. Buyers will often push to reduce it well past what it would cost them to replace the entire roof even if a total replacement is excessive. Ultimately, the decision is up to you, but roof restoration is usually the better option.

Maybe. Rejuvenation restores flexibility to shingles that are showing signs of age, but are still in generally good condition without widespread granule loss, cracks, or missing shingles. Roof Maxx isn’t designed to address widespread rot, major leaks, or structural damage, so you may need to repair these first.

Not directly, but it helps. Government-backed loans like FHA and VA expect a roof in adequate repair with life left in it, and lenders and appraisers view a maintained, warrantied roof more favorably than a neglected one. Some insurers will also offer better rates for a well-kept roof.

With our five-year, transferable warranty, you’ll enjoy the peace of mind that your roof and entire home are protected.